If the traveler goes astray, he needs a guide. This guide for gold is traditionally not inflation, not geopolitical risks, or global economic growth, but the Fed. Despite the general aversion to the precious metal, expressed in the outflow of capital from ETFs in the amount of more than 100 tons over the past four weeks and in the first speculative shorts since 2019, XAUUSD quotes managed to stabilize near the $1,725 per ounce mark. Investors are eagerly awaiting the Fed's rate verdict.

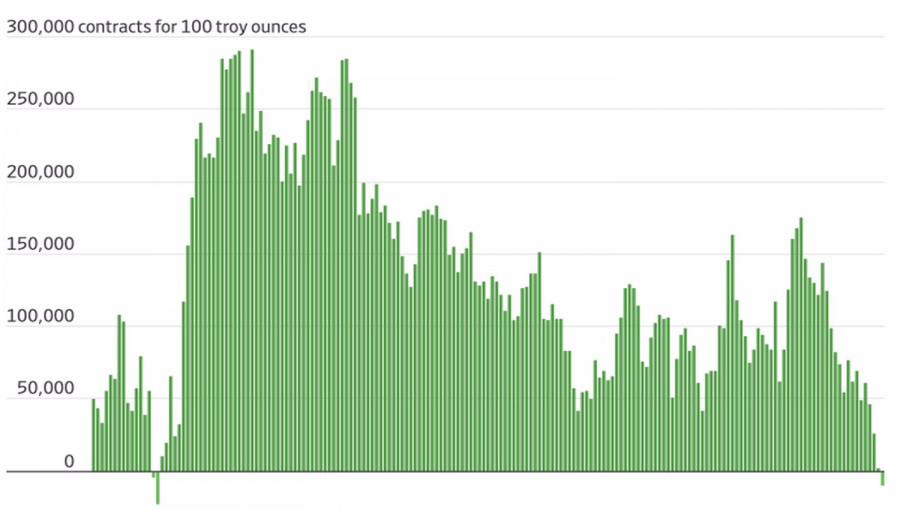

Dynamics of speculative positions in gold

While the latest US macro statistics and comments by FOMC officials have virtually ruled out the possibility of raising the federal funds rate by 100 bps in July, CME derivatives give a 26% chance of such an outcome at the next meeting of the Committee. Investors are interested in what the Fed plans to do in September. Will it follow the ECB's lead into a data-driven policy, or will it continue to use direct guidance? The first option looks bad for the US dollar and good for gold. The second is fraught with new mistakes of the Central Bank but will show its determination in the fight against inflation.

The derivatives market gives a 49% chance of a 50 bps rate hike in September, the probability of its increase by 75 bps is estimated at 42%, while 100 bps is at 9%. Which option will Jerome Powell choose? I believe that his team will focus on incoming statistics. In particular, several reports on the labor market and inflation in the US will see the light before the next FOMC meeting.

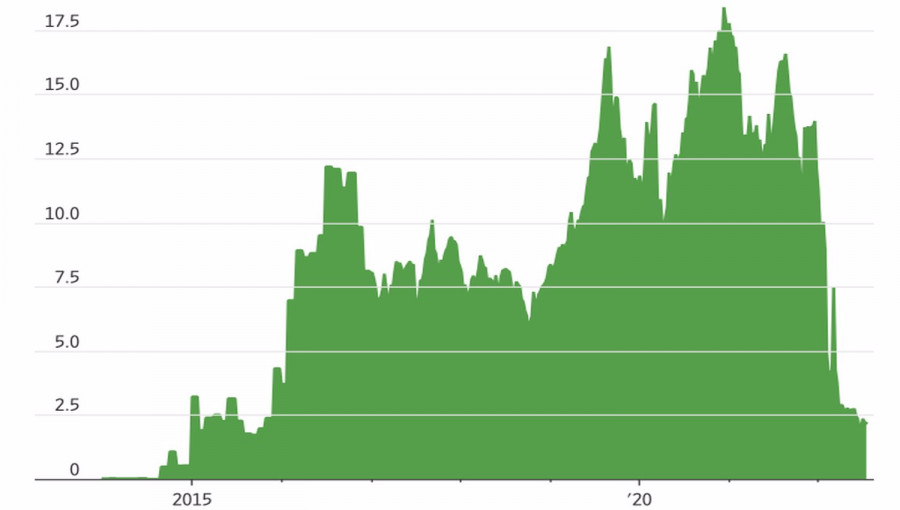

The Fed's verdict will affect not only the dollar, but also the yield of US Treasury bonds, the dynamics of which is sensitive to gold. The fact that more than eight dozen central banks are tightening monetary policy has already reduced the size of the global negative-yielding debt market to $2.4 trillion, down 87% from the $18.4 trillion peak in December 2020. Then gold felt confident trading above $1900 an ounce. Now investors are asking themselves: why hold a non-interest-bearing precious metal in a portfolio when you can buy bonds?

Negative Yield Global Debt Market Dynamics

The XAUUSD bulls have an answer to it. Since the beginning of the year, 10-year US Treasury yields have jumped 84%, reflecting the debacle of the US debt market, the S&P 500 has sunk 17%, and gold has lost just over 6% of its value. The precious metal can be perceived as a portfolio stabilization tool in a pronounced stagflationary environment. So the IMF, in its latest forecast, warned that global GDP could slow to 2.6% in 2022 and—to 2% in 2023%, while inflation in advanced economies will accelerate to 6.6%.

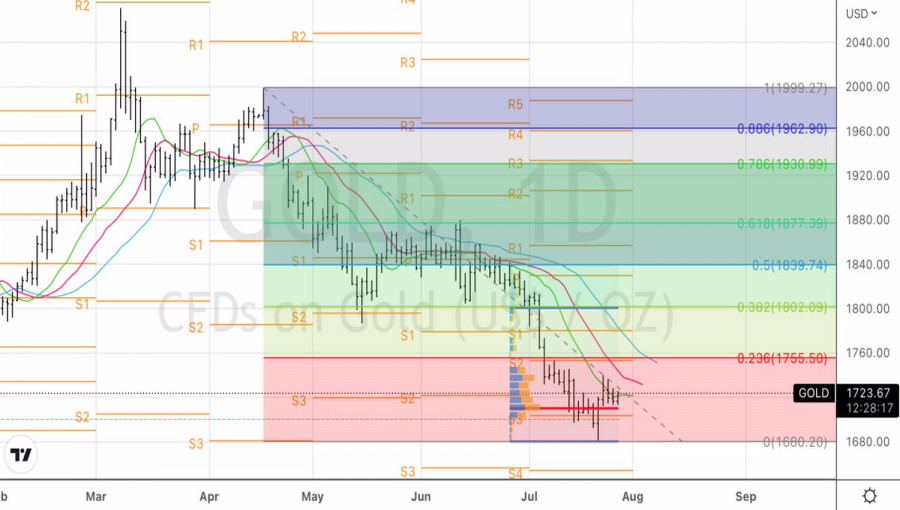

Technically, the fall of gold below the fair value by $1,710 and the pivot point by $1,700 is a reason to sell it as part of Linda Raschke's Holy Grail strategy. It assumes the formation of shorts at the levels of the lows of the dynamic resistance test bar in the form of EMA.

Trading analysis offered by RobotFX and Flex EA.

Source

Please do not spam; comments and reviews are verified prior to publishing.